There has been further developments. Some agitating shareholders holding ~5% of MPS have requested the Responsible Entity (RE - MacarthurCook Fund Management) to organise a meeting of unit holders to vote on the the following proposed changes:

MacarthurCook Fund Management is also the current manager. Given the number of shareholders requesting the meeting, I understand either the RE or shareholders themselves can organise the meeting. The RE has yet to respond, however one would expect an announcement to be made shortly and a meeting date to be set.

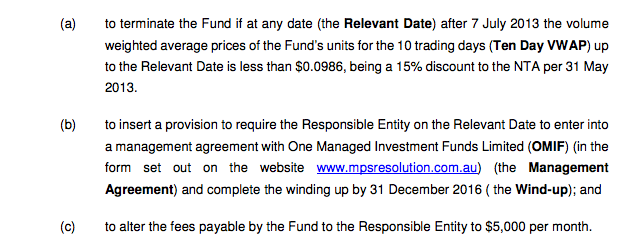

The website (www.mpsresolution.com.au) allows people to download the proposed management agreement with One Managed Investments Funds Ltd, and register their contact details for further information. I have been in contact with some disaffected unit-holders, and have met with Michiel Geerdink who is spearheading the campaign for change. Mr Geerdink informs me that he (or related entities) does not have a financial interest in One'.

Based on the conversations I have had with various people, I believe there is a lot more than 5% of shareholders who are unhappy with current management.

AIMS (the owner of MacarthurCook) holds 26.3% of the shares.

So shareholders will have a choice of sticking with current management or appointing a new manager. What to do? There is only question I am focussed on: who will deliver the greatest Internal Rate of Return (IRR).

Here are some thoughts.

I recently met with management. They have previously articulated the strategy to decrease the gap between the share price and NTA (announcement 3 June):

I would be happy to keep the current management and hold for the long term if I start receiving a healthy level of distributions, and the book value and income payments grow over time. The problem is, I don't know how confident I can be that will happen. I therefore see management as having to rapidly prove itself in this regard.

There is an upcoming meeting to recapitalise the St Kilda Road property. Note this property is also managed by another AIMS fund. Investors hate conflicts of interest - real or perceived - and quite rightly. The conflicts must be addressed, either by removing them, or at least providing a very high level of transparency through regular progress reports. It is not unreasonable to expect regular progress reports on the fund strategy, particularly after full year results have been finalised.

A further capital raising would be disastrous. I would like to see management clarify publicly this will not happen.

An outline of future internal cash-flows and indicative distribution guidance should also be provided. This should include the intentions with ongoing court case legal bills.

As proposed, the other alternative is to simply wind up the fund. One' would have a deadline of 2016, however a chunk of the assets should be paid in the near term. On my ultra crude IRR calculations, realising the investments at NTA would yield well over 20% p.a. on the current price of 7.2c and realising investments at NTA. The primary objection to this strategy is the illiquidity of some of the assets and realising actual NTA may not be possible. Still, even allowing for a haircut of 20% on the assets (ex cash) I get an IRR of 15% p.a. I can't stress enough these are strictly my guesstimates and should in no way be relied upon. The actual sale value and timing of payments will have a substantial impact on IRR. I have no idea of the actual realisable sale value of the assets other using current book value as a guide. Please also note my disclaimer on this blog.

I would like to see the agitating shareholders provide a detailed analysis of the wind-up strategy and projected IRR range at the upcoming shareholders meeting. I think this will greatly assist shareholders in their decision making.

Kristian

Disclosure: own MPS